Updated March 2026 with current Stripe UK pricing.

If you're running a UK business and taking payments online, Stripe is probably on your radar. It's become the default choice for startups and scale-ups alike, thanks to its developer-friendly API and clean dashboard.

But those transaction fees? They add up faster than you might expect. Let's break down exactly what you'll pay with Stripe in the UK and whether there are better alternatives for your business.

What Are Stripe Fees?

Stripe fees are the charges you pay every time a customer makes a purchase through your website, app, or payment link. Think of it as the cost of accepting card payments without the headache of setting up a traditional merchant account.

These fees cover transaction processing, fraud protection, PCI compliance, and access to Stripe's suite of tools. There are no setup fees or monthly charges on the standard plan—you only pay when you process a payment.

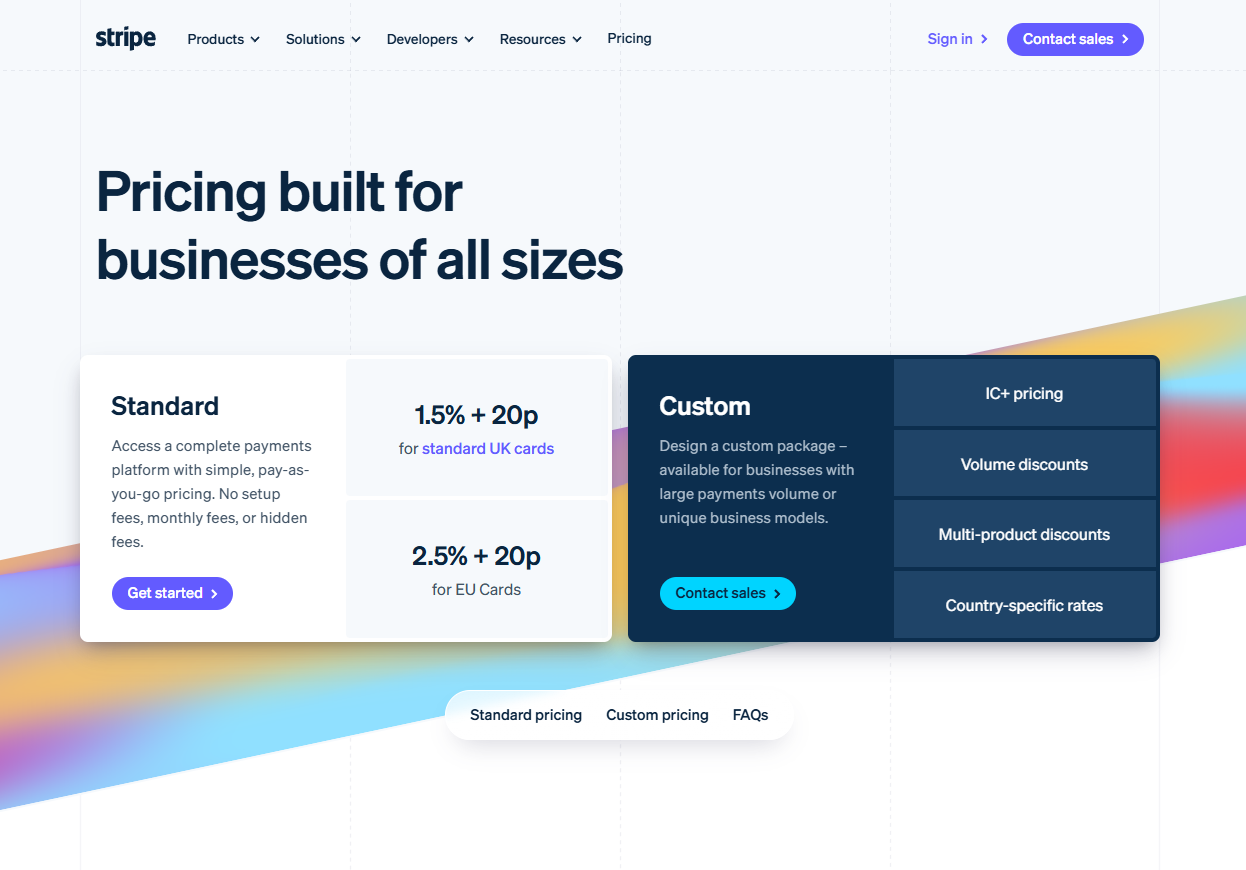

Current Stripe UK Pricing in 2026

Here's the complete breakdown of Stripe's UK transaction fees:

| Payment Type | Fee | Example (£100 sale) |

|---|---|---|

| UK cards (Visa, Mastercard) | 1.5% + 20p | £1.70 fee, £98.30 payout |

| European (EEA) cards | 2.5% + 20p | £2.70 fee, £97.30 payout |

| International cards | 3.25% + 20p | £3.45 fee, £96.55 payout |

| UK Amex | 2.0% + 20p | £2.20 fee, £97.80 payout |

| Premium/Corporate cards | 1.9% + 20p | £2.10 fee, £97.90 payout |

| Stripe Terminal (in-person) | 1.5% + 20p | £1.70 fee, £98.30 payout |

| Currency conversion | +2% | Stacks with card fees |

| Instant payouts | 1% (min 50p) | For same-day access |

| Chargebacks/disputes | £20 per dispute | Charged win or lose |

Post-Brexit Fee Changes

Since June 2024, Stripe has applied a 1.5% fee to payments made using European bank-based methods like SEPA Direct Debit and iDEAL. This reflects the increased costs of cross-border transactions post-Brexit.

For UK businesses with European customers, this is an important consideration when calculating your true payment processing costs.

The Hidden Costs That Add Up

Beyond the headline transaction fees, several other costs can catch you off guard:

Currency conversion fees stack on top of your card fees. If a US customer pays in dollars and you settle in GBP, you're looking at the international card rate (3.25%) plus the 2% conversion fee. That's 5.25% + 20p on a single transaction.

Refund fees aren't refunded. When you refund a customer, Stripe doesn't return the original processing fee. On a £100 refund, you've still lost £1.70.

Chargeback fees apply regardless of outcome. Whether you win or lose a dispute, Stripe charges £20. The average UK business sees a 0.1-0.5% chargeback rate—at 0.2% on £10,000 monthly volume, that's 2-3 chargebacks costing £40-60.

Premium features add up. Stripe Radar for advanced fraud protection costs 5p per transaction. Stripe Billing starts at 0.7% of recurring billing volume. Stripe Invoicing adds 0.4-0.5% per invoice.

Real-World Cost Example

Let's say you're a UK SaaS business processing £20,000 per month with 500 transactions averaging £40 each:

- UK card transactions (80%): £320 in fees (1.5% of £16,000) + £80 (20p × 400) = £400

- European cards (15%): £75 (2.5% of £3,000) + £15 (20p × 75) = £90

- International cards (5%): £32.50 (3.25% of £1,000) + £5 (20p × 25) = £37.50

- Chargebacks (2 disputes): £40

Total monthly fees: ~£567.50, or roughly 2.8% effective rate

That's nearly £6,800 per year. At £50,000 monthly volume, you're looking at over £17,000 annually.

Strong Customer Authentication (SCA) in the UK

One thing UK businesses need to understand is Strong Customer Authentication—a security requirement carried over from PSD2 that became mandatory in March 2022.

SCA requires customers to verify their identity using two of three factors: something they know (PIN or password), something they have (phone or card), or something they are (fingerprint or face ID).

Stripe handles SCA compliance automatically through 3D Secure 2 (3DS2), which adds an authentication step at checkout. While this reduces fraud, it can also increase cart abandonment if not implemented smoothly.

When Should UK Founders Consider Alternatives?

Stripe's convenience comes at a price. Here's when it makes sense to explore other options:

You're Processing High Volumes

Once you're consistently processing over £100,000 monthly, you have leverage. Traditional merchant accounts with interchange-plus pricing often work out cheaper at scale. Stripe does offer custom pricing for high-volume businesses, but you'll need to negotiate.

Most of Your Customers Are International

If a significant portion of your revenue comes from international cards, the 3.25% + 20p rate plus potential currency conversion fees will seriously eat into your margins. Processors like Adyen or Airwallex may offer better rates for international transactions.

You're a Subscription Business

For recurring billing, the base transaction fees plus Stripe Billing's 0.7% can feel heavy. Direct Debit via GoCardless charges just 1% + 20p (capped at £4 per transaction) and has no chargebacks—payments are pulled directly from bank accounts.

You Take In-Person Payments

While Stripe Terminal works well, dedicated POS providers like SumUp (1.69% flat rate) or Square (1.75%) may be more cost-effective depending on your transaction sizes and volumes.

Top Stripe Alternatives for UK Businesses

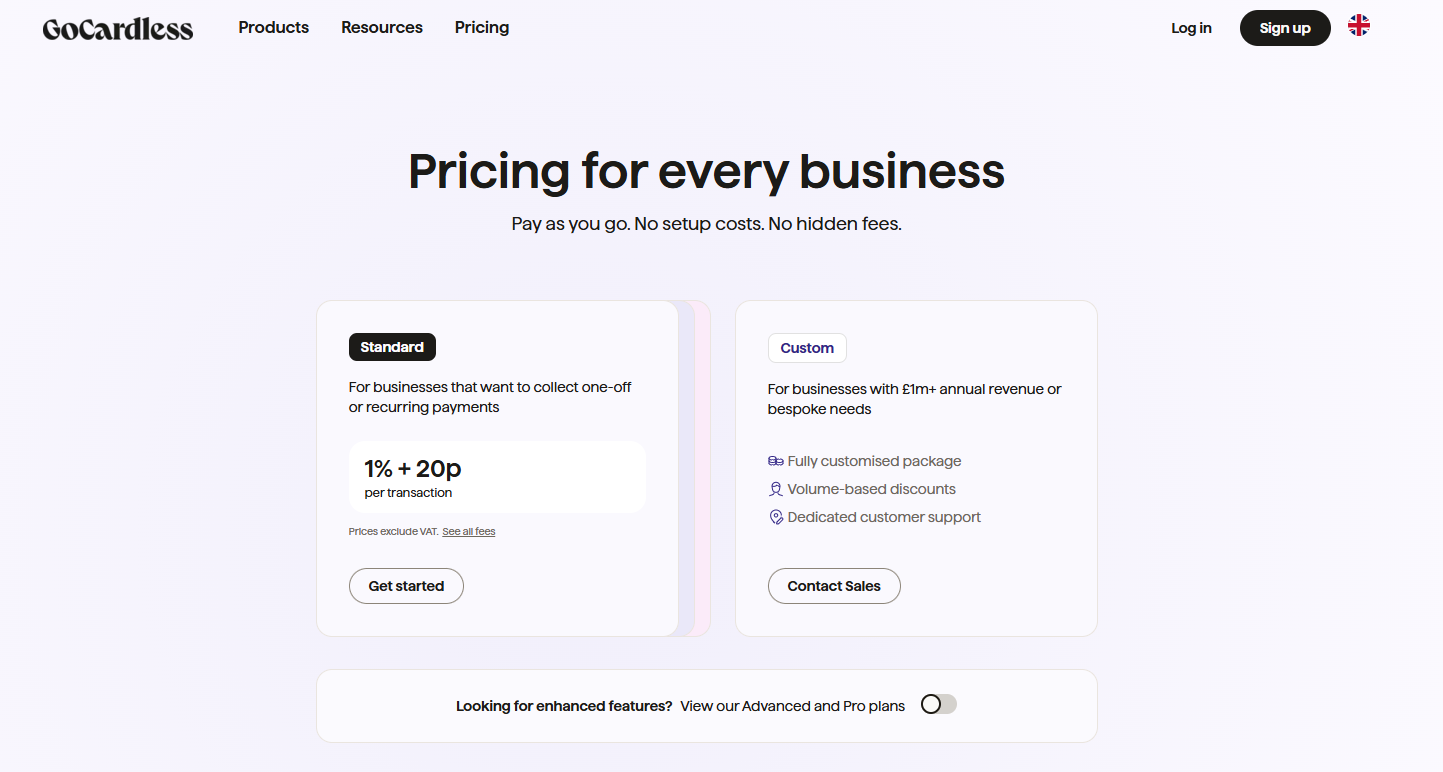

GoCardless (Best for Recurring Payments)

GoCardless specialises in Direct Debit, making it ideal for subscriptions and invoices. UK businesses pay 1% + 20p per transaction, capped at £4 maximum. There are no chargebacks (Direct Debit disputes are rare and handled differently), and payments are guaranteed once collected.

The trade-off: slower settlement times (3-5 days) and customers need to set up a mandate, which adds friction compared to card payments.

Revolut Business (Best for Multi-Currency)

Revolut Business offers payment processing starting at 1% + 20p for UK cards (online), with competitive FX rates at 0.6% above interbank versus Stripe's 2%. For businesses with significant international transactions, the savings can be substantial.

Plans start at £10/month (Basic) up to £90/month (Scale), with varying allowances for free transfers and currency exchange.

SumUp (Best for In-Person)

SumUp charges a flat 1.69% for all in-person card payments with no monthly fees. Hardware starts from £25 for the Solo Lite reader. For businesses processing over £3,000/month in-person, their Payments Plus plan (£19/month) drops the rate to 0.99%.

Online payments are pricier at 2.5%, so SumUp works best as a complement to Stripe rather than a replacement.

Square (Best All-In-One)

Square charges 1.75% for in-person payments and 1.4% + 25p online. Unlike Stripe, Square absorbs chargeback fees—a meaningful benefit for businesses in higher-risk categories like food delivery.

Square also offers free POS software, invoicing, and a business bank account, making it genuinely all-in-one.

Adyen (Best for Enterprise)

For larger businesses processing significant volume, Adyen offers interchange-plus pricing with full transparency on costs. You'll pay the actual interchange fee (set by card networks) plus Adyen's markup, which can work out significantly cheaper than Stripe's blended rates.

The catch: Adyen requires a minimum monthly processing volume and is more complex to integrate.

VAT on Stripe Fees

A quick note on tax: Stripe's processing fees are subject to VAT. If you're VAT-registered, you can claim this back, effectively reducing your net processing cost by 20%.

On £1,000 in Stripe fees, that's £200 back through your VAT return. Make sure your accountant is treating these correctly.

Making the Switch: What to Consider

Before leaving Stripe, think through these factors:

Integration complexity. Stripe's developer experience is genuinely excellent. If you've built custom integrations, switching means development time and potential disruption.

Feature parity. Stripe's ecosystem is vast—subscriptions, invoicing, fraud protection, tax calculation, and more. Ensure your alternative covers everything you use.

Customer experience. Some alternatives don't offer the same smooth checkout experience. Test thoroughly before committing.

Support quality. Stripe's documentation and support are industry-leading. Check reviews for your alternative's support experience.

The Bottom Line for UK Founders

Stripe's 1.5% + 20p headline rate is competitive for UK domestic transactions. For early-stage startups, the zero setup costs, no monthly fees, and excellent developer tools make it an easy choice.

But as you scale, those fees become a significant line item. A business processing £500,000 annually at an effective 2.5% rate is paying over £12,500 in processing fees—enough to fund a marketing campaign or part of a salary.

The key is timing. Don't optimise prematurely when you should be focused on growth. But once payment processing becomes one of your top five expenses, it's worth doing the maths.

Start by calculating your actual effective rate (total fees ÷ total revenue processed). If it's significantly above the headline 1.5%, you likely have international customers, refunds, or chargebacks inflating your costs—and alternatives might offer real savings.